Electricity Industry Faces Risks from Three New Technologies

Electric company annual reports describe technological risk in the vaguest of terms, asserting that firms face numerous, generalized risks— boiler plate to provide legal cover just in case something happens, such as an ET invasion. What specific risks do the companies face? You’ll never know from reading their reports. Anyway, it often takes years for something to happen in the utility industry, so why bother worrying now? Brokerage reports, generally optimistic, focus on a utility’s rate base growth (mostly their assets), AI demand, ongoing regulatory complacency all within a 3-5 year horizon. Technological disruption of business that may be 5-10 years out seems beyond the decision time horizon of big investors. They can always sell out ahead of time, right? “What, me worry?” sums up the picture, aided by lofty market valuations.

This relaxed attitude of utilities toward technology risk and their present business makes little sense for three reasons. First, tech innovation can sneak up faster than expected, so the investor (the capital provider) might not have enough time to exit in an orderly fashion, and the company might not have enough time to prepare to deal with the financial disruption. Second, a likely or probable event even five years in the future affects the value of utility capital investments made today that have expected 20-30 year lives. Third, the utility industry overall pays so little attention to science and technology (it spends a pathetic 0.1% of revenues on R&D) that it may be the last to know when new technologies are about to emerge and disrupt their business. We could go into other reasons why the industry and its investors will tardily perceive or act on risks, including herd mentality, cultural issues, indexing, paradigm shifts, and regulation, but why bother? Simply put, we think that emerging technological developments, all staring us in the face right now, could start to disrupt the electricity industry’s structure and market in the coming 5-10 years. This should affect the industry’s financing picture even sooner. Investors will react to possible adverse business developments sooner than entrenched utility managers and quickly reflect those new worries about the industry’s declining prospects into stock prices and interest rates. Related: US Crude Oil, Gasoline Inventories Continue to Crash as Iran War Takes Its Toll

Before going on, though, let’s accept two academic definitions of risk: either the possibility of loss or the possibility that actual returns will not rise to expected levels. If your investment cannot earn its expected return, it probably will decline in value, whether you sell it or not, so the second definition really says the same thing as the first, but less directly.

Now, let us examine a trio of obvious risks. There are more, of course.

Risk one: Batteries

Batteries have already changed the electricity industry, reducing the need for transmission and redundant generating capacity and enabling the industry to treat renewable resources in the same way as ordinary generation. We expect more change and not just from lower costs. The battery industry suffers from massive overcapacity while in the midst of a huge product improvement program. Surely it will seek more markets, with residential and small commercial customers as likely targets. They consume over half the electricity output and pay the highest prices of any customer class. Imagine combining inexpensive solar (see RISK TWO) with inexpensive, compact, safe storage. Many customers, especially in rural areas, might finally cut the cord that ties them (expensively) to the electrical grid. If enough customers begin to exit and self generate, the grid will become more and more a provider of last resort for those who cannot install or afford to own their own on-site equipment, in other words, small and low income consumers. This prospect should really alarm public policy makers. A grid with a shrinking customer base of this sort is likely to require meaningful government support (or face financial distress). We’d bet on commercial development of low cost, small residential and commercial batteries within five years.

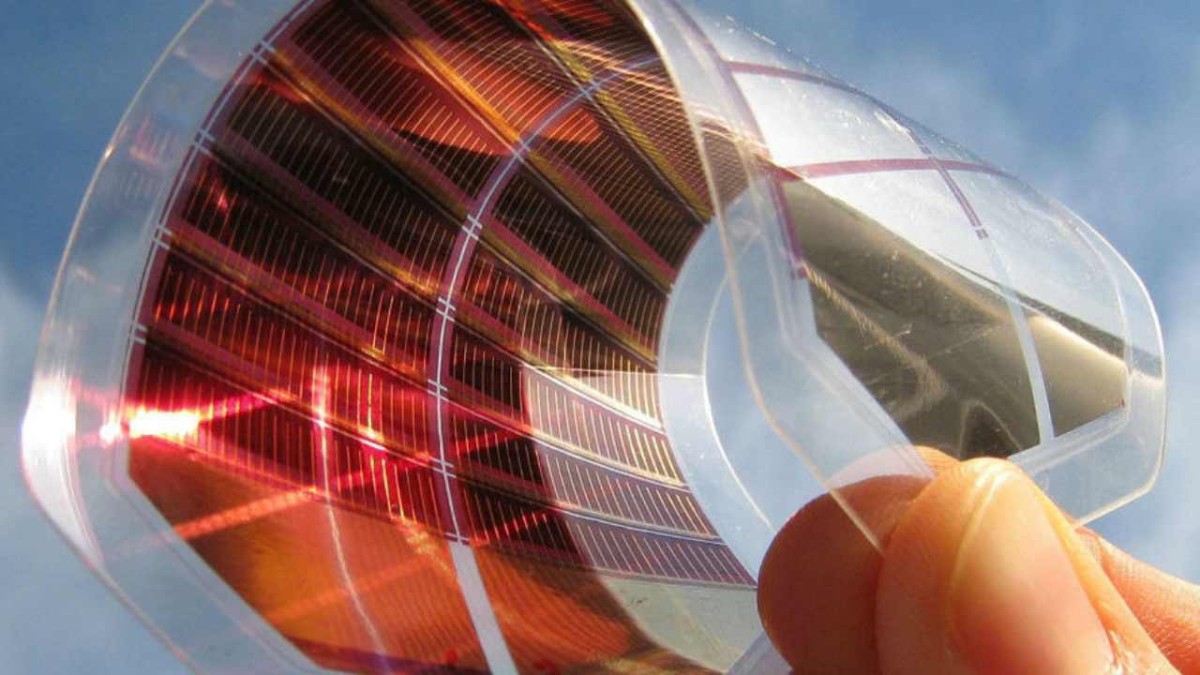

Risk Two: Perovskites

Photovoltaic cells made with perovskite mineral compounds are more efficient than silicon cells but they are not as durable and have not achieved flexibility targets. Manufacturers and researchers have launched an impressive effort to solve those problems in order to produce high efficiency, durable, and flexible perovskite cells within a few years. These improvements will do more than increase the efficiency of the cells. Buyers of the new flexible cells could install them anywhere, wrap them around buildings, put them in window blinds or even on clothes, making the perovskite cells ubiquitous. Think about it. The new cells will produce 30-50% more electricity per cell than the old ones, and wrapping an entire building might increase installation surface by 50-100%. That would permit twice the power production on the site. Combined with a low cost battery, the perovskite cell will make off-the-grid electricity even more attractive. Is this science fiction? No, read the technical papers. Commercialization seems likely within five years.

Risk Three: Nuclear Fusion

Privately financed firms have announced plans to build fusion reactors within 5-10 years — plants roughly the size of planned small modular reactors (SMRs) which will, supposedly, enter commercial operation within the same time period. SMRs are like present day fission reactors, just smaller, with a modular build out, and even more expensive than current gigawatt scale nuclear designs. And, if you don’t like existing nukes for environmental, national security, ideological or safety reasons, you probably won’t like SMRs, either. However, fusion reactors won’t require uranium, emit carbon dioxide, produce long-lived radioactive wastes, enable nuclear proliferation and can’t melt down — a list which might convince even hard core anti-nuclear activists to give them a pass. Fusion is nuclear power without the baggage. (And it's not based on a recycled submarine propulsion technology either.) It does not present a threat to central station electricity, per se, but rather to SMR development (fusion and SMRs are competitors) and ultimately to fossil-fueled power plants which fusion could replace. Opponents of renewables insist that the country and the utility industry need base load power plants. Fusion could provide base load power without either carbon dioxide emissions or the nuclear fission liabilities. Of course, fusion is all talk, right now but as we previously pointed out, a lot of new capital is entering the field. If it should work, and produce competitively priced electricity, though, the age of electrification will really come. Renewables and fusion reactors would power the economy. But that seems unlikely for at least a decade. Best advice: rest easy but be wary.

Why Worry?

Admittedly, we did not discuss all technological risks, such as plug-in solar (already big in Europe), which will dampen utility sales, or solar power satellites (a goal for billionaire space entrepreneurs), which could upend the generation market. You can never tell what will come along. Nor did we consider the risks to the natural gas industry, which are substantial, given that electric generators consume 40% of gas sold, and that is the only gas market that has shown any dynamism. Technological innovation in the electricity sector (mostly batteries right now) will reduce natural gas sales to the power sector and sales of gas for heating and cooking, too. The natural gas industry will have to export a lot of gas to make up for those losses. Then there is the impact of tech change on the consumption patterns of high-tech electricity users. Try this one. Quantum computers or space-based computer centers render earth-bound AI obsolete. For that matter, what might happen if the next administration in Washington takes environmental issues seriously, thereby forcing tech change on the industry? And finally, we admit it, we did not discuss technological changes that might offset the risks posed in this essay, or technological changes that might boost industry prospects. That is because risk was the topic. Anyway, everyone touts the benefits, so they probably are in the stock prices.

Finally, why worry? The short answer is that the utility industry we know is fragile in ways we don’t often talk about. Capital-intensive industries are often like that. So, how about this back- of- the -envelope calculation that takes into account that much of the industry’s costs are fixed, that is, won’t decline proportionately with the loss of sales. We concluded that a 5% loss of residential and commercial sales (if consumers deserted the grid) could reduce electric company pretax net income by 15-20%. Plus, the now distressed utility would also have to account for losses on assets rendered redundant after a meaningful decline in sales. (These are not assets that could be transferred to an AI customer.) Finally, consider that once a consumer trend begins, and people see that their neighbors are on board, the trend can snowball. In other words, 5% may be the beginning. We have repeated here a form of the utility “death spiral" argument to show how these new and emerging technologies represent a real and persistent threat to future utility revenues and business prospects.

This discussion may sound like science fiction to you, an inventory of non-existent risks based on academic musings and commercial hyperbole, but we already live in a world resembling that of science fiction: rockets to the moon, autonomous vehicles, thinking machines, people with mechanical parts. So, what is so outlandish about people making their own electricity from the sun, storing it in boxes, or producing power in machines fueled by products extracted from water and left over from a nuclear reaction. And what are the risks of those technologies to a nineteenth-century industry model? We may find out sooner than you expect.

More Top Reads From Oilprice.com

More Top Reads From Oilprice.com